Income Tax Calculator for Germany

Navigating the German tax system can often feel like one of the most significant hurdles when settling into life in Germany. The bureaucracy, the unfamiliar terminology, and the sheer number of rules can be intimidating for even the most seasoned expatriate. However, understanding this system is not just a necessity—it’s an opportunity to optimize your finances and ensure you are taking full advantage of the benefits available to you.

Fortunately, the landscape for taxpayers in Germany has seen positive developments. For the 2025 tax year, the German government has enacted several relief measures designed to put more money back into the pockets of residents. The cornerstone of this relief is a significant increase in the basic tax-free allowance, meaning a larger portion of your hard-earned salary is protected from taxation before the progressive rates even begin to apply.

This guide is designed to be your one-stop, comprehensive resource for demystifying German income tax in 2025. We will break down everything an expatriate needs to know, from the fundamental tax rates and the all-important choice of your tax class (Steuerklasse) to the specific allowances for families, surcharges, filing requirements, and special considerations that are particularly relevant to the international community. This report provides an accurate, up-to-date, and exhaustive overview to help you navigate your German financial obligations with confidence.

The Foundation: Germany’s Income Tax System Explained

At its core, the German income tax system is built on two key principles: protecting a basic subsistence minimum from taxation and applying a progressive rate to income earned above that minimum. Understanding these two concepts is the first step to mastering your finances in Germany.

How German Income Tax Works: The Principle of the Tax-Free Minimum

The bedrock of the German tax system is the Grundfreibetrag, or the basic tax-free allowance. This is not merely a tax loophole but a constitutionally protected principle ensuring that the state does not tax the income required for basic subsistence—the money needed for essentials like food, housing, clothing, and medical care.

For the 2025 tax year, the Grundfreibetrag is set at €12,096 for a single individual. For married couples or registered partners who file their taxes jointly, this amount is doubled to €24,192.

This means that you do not pay any income tax on earnings up to this threshold. The tax calculation only begins on the first euro you earn above this amount. This allowance is applied automatically by the tax authorities (Finanzamt) and your employer’s payroll department; you do not need to apply for it. This allowance has been steadily increasing, with a retroactive increase for 2024 raising it to €11,784 from an initial €11,604, providing tangible relief to taxpayers.

German Income Tax Brackets: The Progressive Rate

Once your income surpasses the Grundfreibetrag, Germany applies a progressive tax system. In simple terms, this means that the rate of tax increases as your income rises. This ensures that individuals with a higher ability to pay contribute a larger percentage of their income in taxes.

The income tax brackets are structured as follows:

| Tax Rate | Taxable Income (Single Filer) | Taxable Income (Married Filing Jointly) |

|---|---|---|

| 0% | Up to €12,096 | Up to €24,192 |

| 14% to 42% (Progressive) | €12,096 – €68,481 | €24,192 – €136,962 |

| 42% | €68,481 – €277,826 | €136,962 – €555,652 |

| 45% | Over €277,826 | Over €555,652 |

Source:

Federal Ministry of Justice and Consumer Protection (German only)

vermoegenszentrum.de (German only)

A crucial nuance lies within the second bracket, which spans from €12,096 to €68,481. The rate is not a flat 14% but is described as “geometrically progressive”. This means that the marginal tax rate—the rate you pay on each additional euro earned—increases smoothly and continuously throughout this bracket. It does not jump abruptly at certain thresholds. For example, a person earning €30,000 will have a lower average and marginal tax rate than someone earning €60,000, even though both fall within the same bracket. This sophisticated calculation, managed by a complex formula, prevents the kind of unfairness seen in simpler systems where earning one extra euro could push you into a much higher tax bracket for a large chunk of your income. It ensures a fairer, more gradual increase in the tax burden.

The top rate of 45%, applied to very high incomes, is often referred to as the Reichensteuer, or “wealth tax”.

Beyond Income Tax: Understanding Surcharges and Other Key Taxes

Your total tax burden in Germany is not limited to the income tax (Einkommensteuer). Several other taxes and surcharges can apply, depending on your income, religious affiliation, and financial activities. Understanding these is essential for a complete picture of your fiscal responsibilities.

The Solidarity Surcharge (Solidaritätszuschlag or Soli): A Tax That’s Mostly History

The Solidarity Surcharge, or Soli, was introduced in the 1990s to cover the costs of German reunification. For decades, it was a standard 5.5% levy on top of the income tax owed. However, since January 2021, the Soli has been eliminated for approximately 90% of all taxpayers, providing significant relief for low and middle-income earners.

It is critical to understand that the Soli is calculated as 5.5% of your income tax liability, not your gross income. You only pay it if your income tax bill exceeds a certain threshold. For 2025, these thresholds have been raised again:

- Single Filers: No Soli is due if your annual income tax is below €19,950.

- Joint Filers: No Soli is due if your annual income tax is below €39,900.

For those whose income tax liability is just slightly above these thresholds, the full 5.5% is not charged immediately. Instead, there is a “transition zone” (Milderungszone) where the surcharge is phased in gradually to prevent a harsh tax cliff. The consistent raising of this exemption threshold demonstrates a clear policy of phasing out the Soli for all but the highest earners.

| Year | Exemption Threshold (Single) | Exemption Threshold (Joint) |

|---|---|---|

| 2023 | €17,543 | €35,086 |

| 2024 | €18,130 | €36,260 |

| 2025 | €19,950 | €39,900 |

| 2026 | €20,350 | €40,700 |

Church Tax (Kirchensteuer): The Optional Contribution

In Germany, officially recognized religious organizations are granted the status of public-law corporations, which allows them to levy a tax on their registered members to fund their activities. This is known as Kirchensteuer, or church tax. This applies primarily to members of the Protestant and Catholic churches, as well as Jewish communities.

The tax rate is either 8% of your income tax liability in the states of Bavaria and Baden-Württemberg, or 9% in all other German states. Like the Soli, this is a percentage of the income tax you owe, not your gross salary. For example, if your annual income tax is €10,000 and you live in Berlin (9% rate), your church tax would be €900.

For many expats, this tax comes as a surprise. When you register your address in Germany (Anmeldung), you will be asked about your religious affiliation. If you declare yourself as a member of one of these tax-levying communities, you will be automatically enrolled to pay church tax.

How to Opt-Out: If you are not an active member of a church or do not wish to contribute, you can formally opt-out. This process is called Kirchenaustritt (leaving the church). It requires a formal declaration at a local government office, typically the Amtsgericht (local court) or Standesamt (registry office), depending on the municipality. This process is usually quick but may involve a small administrative fee, ranging from €25 to €100. This is a crucial piece of actionable advice for new arrivals.

It is also worth noting that the church tax system contains a built-in relief mechanism. The full amount of church tax you pay in a year is considered a “special expense” (Sonderausgabe) and is fully deductible from your taxable income for the following year. This creates a small feedback loop: paying church tax reduces your taxable income, which in turn slightly lowers your income tax liability, and consequently, the basis on which the next year’s church tax is calculated. This means the effective rate is always slightly lower than the nominal 8% or 9%.

A Brief Look at Other Taxes Relevant to Expats

To provide a complete financial overview, several other taxes are pertinent to expats in Germany:

- Capital Gains Tax (Abgeltungsteuer): Income from investments, such as interest, stock dividends, and profits from selling shares, is subject to a flat tax rate of 25%, plus the solidarity surcharge (if applicable) and church tax (if applicable). There is an annual tax-free allowance for capital gains income of €1,000 for single individuals and €2,000 for married couples.

- Trade Tax (Gewerbesteuer): This tax is highly relevant for anyone who is self-employed or operates a business in Germany. It is a municipal tax levied by the local authority where the business is located, so the rate varies. The base federal rate is 3.5%, which is multiplied by a municipal factor (Hebesatz), resulting in effective rates typically between 7% and 17%. Individuals and partnerships benefit from a tax-free allowance of €24,500 on their business profits before this tax applies.

- Value-Added Tax (VAT) (Umsatzsteuer): This is the standard sales tax applied to most goods and services. The standard rate is 19%, with a reduced rate of 7% applied to essential items like most food products, books, and public transport. Freelancers and businesses with revenues above a certain threshold must charge VAT to their clients and remit it to the tax office.

The Expat’s Most Important Choice: Your Tax Class (Steuerklasse)

Perhaps the most confusing, yet financially significant, concept for expats to grasp is the German system of tax classes, or Steuerklassen. Your assigned tax class has a direct impact on your monthly net salary. For married couples, making the right choice can mean a difference of hundreds of euros in take-home pay each month.

What Are Tax Classes and Why Do They Matter?

It is essential to understand what tax classes do—and what they don’t do. A common misconception is that different tax classes have different tax rates. This is incorrect. The purpose of the Steuerklasse system is to determine the amount of income tax (Lohnsteuer) that is withheld from your monthly salary by your employer.

Your final, actual tax liability for the entire year is calculated only when you file your annual tax return (Steuererklärung). The tax class system is simply a method of pre-paying that estimated annual liability in monthly installments. The key difference between the classes is which tax-free allowances—such as the basic allowance (Grundfreibetrag), child allowances, and single-parent relief—are factored into your monthly payroll calculation. Choosing a different class combination shifts these allowances between partners, altering monthly cash flow but not the total tax owed at the end of the year.

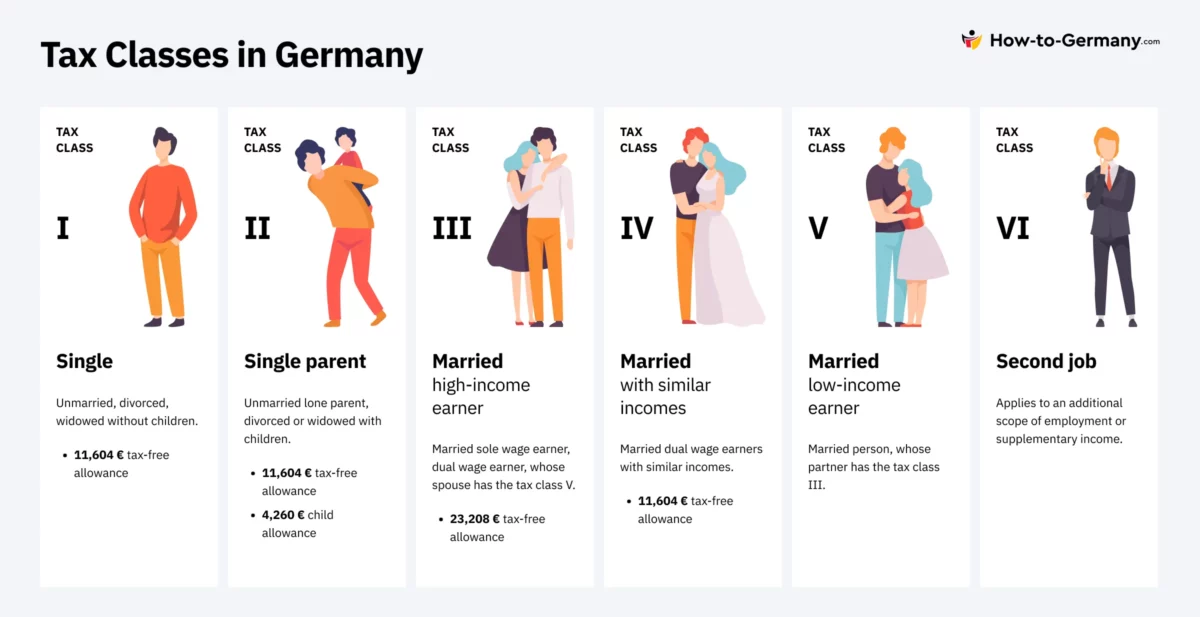

The Six German Tax Classes: A Detailed Breakdown

The Finanzamt assigns a tax class based primarily on your family status. For single individuals, the class is fixed, but for married couples, there is a crucial choice to be made.

| Tax Class | Who It’s For |

|---|---|

| Class I | This class is for single, widowed (after the first year following the spouse’s death), divorced, or permanently separated individuals. It also applies to married individuals whose spouse resides outside the EU/EEA. |

| Class II | This class is designated for single parents who live in the same household with their child and are eligible for the single-parent relief amount (Entlastungsbetrag für Alleinerziehende). |

| Class III | This class is typically chosen by the higher-earning partner in a marriage or registered partnership, or the sole earner. Their partner must then be in Tax Class V. This combination is beneficial when there is a significant income disparity between spouses. |

| Class IV | This is the default tax class for married or registered partners who both earn an income and have similar salaries. Both partners are placed in this class and are taxed as if they were single for withholding purposes. |

| Class V | This class is the mandatory counterpart to Tax Class III and is for the lower-earning partner in a marriage or registered partnership where the other partner has opted for Class III. |

| Class VI | This tax class applies to any income earned from a second or subsequent job. It has the highest deductions because no tax-free allowances are considered. |

A Strategic Guide for Married Expats: Choosing Your Tax Class Combination

For married expats living and working in Germany, the choice of tax class combination is a strategic financial decision. It boils down to a trade-off between maximizing monthly cash flow and ensuring certainty at the end of the tax year. There are two primary combinations to consider.

Combination 4/4: The “Safe and Simple” Option

This is the default combination assigned to married couples when both partners are employed. It is most suitable when both partners earn roughly similar incomes, typically where the income split is no greater than 60/40. In this setup, each partner’s monthly withholding is calculated as if they were single (Class I), meaning each gets their own standard tax-free allowance applied to their payroll.

- Result: The monthly tax deductions are relatively accurate and fair for both partners. When you file a joint tax return, you often receive a refund because the combined calculation is more favorable than the two separate monthly calculations.

- Filing Obligation: With the standard 4/4 combination, filing an annual tax return is generally not mandatory, though it is highly recommended to claim a likely refund.

Combination 3/5: The “Cash Flow” Option

This combination is designed for couples with a significant income disparity, where one partner earns substantially more than the other (typically a 60/40 split or greater).

- Mechanism: The higher-earning partner takes Tax Class III, and the lower-earning partner takes Tax Class V. The core of this strategy is that the entire joint tax-free allowance (€12,096 in 2025) is allocated to the Class III partner’s salary, while the Class V partner receives no tax-free allowance in their monthly payroll calculation.

- Result: The Class III partner’s taxable income is dramatically reduced, leading to much lower monthly tax deductions and a significantly higher net salary. Conversely, the Class V partner’s salary is taxed heavily from the first euro, resulting in a low net income. The overall effect is a substantial increase in the household’s total monthly take-home pay and liquidity.

- Filing Obligation: Choosing the 3/5 combination makes filing a joint annual tax return absolutely mandatory.

While the 3/5 combination is popular for its immediate cash flow benefits, it contains a significant pitfall that can catch unprepared expats by surprise. The higher monthly net income does not represent tax savings; it is effectively an interest-free loan from the tax office. The system is front-loading your tax relief based on an estimate. When you file your mandatory joint return, the Finanzamt calculates the actual tax owed based on your total combined annual income. Because the monthly withholdings in the 3/5 system are often too low compared to this final liability, many couples face a large, unexpected tax bill (Nachzahlung) that can amount to thousands of euros. This “trap” can be a major financial and psychological shock. Therefore, couples choosing this option must be disciplined and set aside money each month to cover the anticipated year-end payment.

Special Tax Class Rules for Expats with a Spouse Abroad

A little-known but hugely beneficial rule exists for expats from EU/EEA countries whose spouse and family have not yet relocated to Germany. Normally, an employee whose spouse lives abroad is placed in Tax Class I, which offers no marital benefits.

However, under specific conditions, an EU/EEA national working in Germany can apply for the highly favorable Tax Class III, even while their spouse remains in their home country. This is possible if one of the following criteria is met:

- At least 90% of the couple’s total worldwide income is subject to German taxation.

- The income earned by the non-resident spouse in their home country is below the German basic tax-free allowance for a single person (or the joint allowance, depending on interpretation and specific treaties).

This requires a formal application to the Finanzamt, including official proof of the spouse’s low or non-existent income from their home country’s tax authority. For many expats in their first year, securing this classification can result in a dramatic increase in their monthly net income.

Maximizing Your Net Income: Key Family Allowances and Deductions

Germany offers generous support for families with children, primarily through a dual system of direct cash payments and tax allowances. Additionally, mandatory social security contributions, while significant, are also largely tax-deductible, further reducing your overall tax burden.

For Expat Families: Kindergeld vs. Kinderfreibetrag

The German state supports families through two main mechanisms: the Kindergeld (child benefit) and the Kinderfreibetrag (child allowance). The system is designed so that every family automatically receives whichever option is financially more advantageous for them.

- Kindergeld (Child Benefit): This is a direct cash payment made to parents each month to help cover the costs of raising a child. For 2025, the Kindergeld is a uniform €255 per month for each child. It is considered an advance payment on the total tax relief you are entitled to for having children.

- Kinderfreibetrag (Child Allowance): This is a tax deduction that reduces your total taxable income. For 2025, the total allowance is €9,600 per child for a jointly assessed couple. This amount is composed of two parts:

- €6,672 for the child’s basic needs (sächliches Existenzminimum).

- €2,928 for care, education, and training needs (BEA-Freibetrag).

The Günstigerprüfung (More Favorable Check): You do not need to choose between these two benefits. When you file your annual tax return, the Finanzamt performs an automatic check called the Günstigerprüfung. It calculates the tax savings you would receive from applying the Kinderfreibetrag. If this tax saving is greater than the total Kindergeld you received during the year (12 x €255 = €3,060), the tax office will apply the allowance to your tax calculation. If the Kindergeld is more beneficial (which is typically the case for lower and middle-income families), the allowance is disregarded. You are always given the better of the two outcomes automatically.

However, a critical piece of advice for all new expat parents is that this automatic system has one manual prerequisite. While the tax office’s Günstigerprüfung is automatic, the monthly payment of Kindergeld is not. You must proactively apply for Kindergeld at the responsible Familienkasse (Family Benefits Office) upon registering in Germany. The tax office performs its year-end calculation under the assumption that you have received the Kindergeld you were entitled to, whether you actually applied for it or not. If you fail to apply, you will not receive the monthly cash payments, and at year-end, the tax office will still factor in the Kindergeld you should have received when determining your final tax bill. This can result in losing out on thousands of euros in support.

Support for Single Parents: The Relief Amount (Entlastungsbetrag)

Germany provides additional tax relief for single parents to help offset the higher costs associated with running a household alone. This is known as the Entlastungsbetrag für Alleinerziehende (relief amount for single parents).

To qualify, you must be single, live in the same household as at least one child, and be entitled to Kindergeld or the Kinderfreibetrag for that child.

- The relief amount for 2025 is €4,260 per year for the first child.

- This amount increases by an additional €240 for each subsequent child.

This relief can be claimed in two ways:

- Proactively: By applying for Tax Class II. This ensures the relief amount is factored into your monthly payroll, increasing your net pay throughout the year.

- Retroactively: By claiming it on your annual tax return. This is done by filling out the “Anlage Kind” (Child Annex) form.

Mandatory Social Security Contributions

A significant portion of your gross salary (Brutto) in Germany is deducted for mandatory social security contributions before you receive your net pay (Netto). These contributions fund Germany’s robust social welfare system. The costs are generally split 50/50 between the employee and the employer. While these deductions are substantial, they are also largely tax-deductible as special expenses, which lowers your final income tax bill.

| Insurance | Employee Contribution Rate (Approx.) | Annual Income Ceiling (2025) |

|---|---|---|

| Pension Insurance (Rentenversicherung) | 9.3% | €96,600 |

| Health Insurance (Krankenversicherung) | 7.3% + supplementary rate (avg. ~1.7%) | €66,150 |

| Unemployment Insurance (Arbeitslosenversicherung) | 1.3% | €96,600 |

| Long-Term Care Insurance (Pflegeversicherung) | ~1.7% (varies by children/state) | €66,150 |

Source:

VDEK (German only)

Contributions are only levied on income up to the specified annual ceiling (Beitragsbemessungsgrenze). Any income earned above this ceiling is not subject to further social security deductions.

Filing Your Taxes: The Steuererklärung for Expats

The annual tax return, or Steuererklärung, is the process through which your final tax liability is reconciled with the amount you have pre-paid via monthly withholdings. For some, it is mandatory; for others, it is a highly recommended opportunity to receive a refund.

Do You Need to File a Tax Return?

While many salaried employees in simple situations are not required to file, for most expats, filing is either mandatory or highly advantageous. Filing a tax return is mandatory if any of the following conditions apply to you during the tax year:

- You are a married couple using the Tax Class combination III/V or IV with Factor.

- You are registered as self-employed (selbstständig) or a freelancer (freiberuflich).

- You received more than €410 in untaxed income or benefits, such as unemployment benefits, short-term work benefits (Kurzarbeitergeld), or parental allowance (Elterngeld).

- You earned income from more than one employer simultaneously, and the second job was taxed under Tax Class VI.

- You received other income not subject to wage tax withholding, such as rental income.

- The tax office has noted a loss carryforward from a previous year on your record.

Even if none of these apply, it is almost always worthwhile for employees to file a return voluntarily. Most employees who file receive a tax refund, often averaging around €1,000, by claiming various work-related expenses, special expenses, and other deductions not accounted for in monthly payroll.

Important Deadlines and Penalties

The German tax year corresponds to the calendar year, and the deadlines for filing your return are strict.

- If you file the return yourself, the deadline is typically the 31st of July of the following year.

- If you use a certified tax advisor (Steuerberater) or a tax assistance association (Lohnsteuerhilfeverein), the deadline is automatically extended, usually to the end of February of the year after next. For example, the return for the 2025 tax year would be due at the end of February 2027.

Failing to meet these deadlines can result in penalties. Late filing may incur a fine of 0.25% of the assessed tax for each month of delay, while late payment of taxes owed is penalized with 1% of the outstanding amount per month.

A Special Note for American Expats

American citizens face a unique situation as the U.S. taxes its citizens on their worldwide income, regardless of where they live. This creates a dual filing obligation: you must file a tax return in both Germany and the United States. To prevent double taxation, the U.S. tax code provides two primary tools: the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC).

While the FEIE allows you to exclude a large portion of your foreign-earned income from U.S. taxation up to an amount that is adjusted annually for inflation, in a high-tax country like Germany, the Foreign Tax Credit (FTC) is often the more strategic choice.

The reason lies in the comparison of tax rates. Germany’s income tax rates are generally higher than U.S. rates for most middle and upper-income levels. The FTC allows you to take a dollar-for-dollar credit for the income taxes you have paid to Germany and apply it against your U.S. tax liability on that same income. Because your German tax bill will almost certainly be higher than what you would have owed in the U.S. on that income, the FTC will typically eliminate your U.S. tax liability entirely. Furthermore, any “excess” tax credits (the amount by which your German taxes exceeded your U.S. liability) can be carried forward for up to ten years to offset future U.S. tax obligations. The FEIE offers no such carry-forward benefit, making the FTC a more powerful long-term financial planning tool for most American expats in Germany.

Conclusion: Your German Tax Checklist and Next Steps

Understanding the German tax system is a journey, but with the right knowledge, it is entirely manageable. The system, while complex, is logical and contains numerous provisions to support residents, particularly families. By being proactive and informed, you can ensure your financial affairs are in order and optimized for your specific situation.

To conclude, here is a simple checklist of the most critical, actionable steps for any expatriate navigating taxes in Germany:

- Check Your Tax Class: If you are married, immediately review your tax class (Steuerklasse) combination. Use a reliable online calculator or consult an advisor to determine if the 4/4 or 3/5 combination is right for your household’s income split. Making the correct choice is the single biggest lever for managing your monthly net income.

- Apply for Kindergeld: If you have children, make it a top priority to apply for the monthly child benefit as soon as you have completed your address registration (Anmeldung). Do not assume this is automatic; failure to apply means losing out on significant financial support.

- Opt-Out of Church Tax: During your Anmeldung, you will be asked about your religion. If you are not an active, practicing member of a tax-levying church, be prepared to state this or take the formal step of Kirchenaustritt to avoid the 8-9% church tax.

- Know Your Filing Deadline: Mark your calendar. The standard deadline is July 31st of the following year. If you anticipate a complex return or simply want more time, engage a tax advisor (Steuerberater) well in advance to secure an automatic extension.

- Consider Professional Advice: For any situation that goes beyond a single, simple salary—such as freelancing, multiple income sources, significant investments, or cross-border spousal income—hiring a certified tax advisor is a wise investment. They can navigate the complexities of the German tax code to ensure compliance and maximize your returns, providing invaluable peace of mind.

Armed with this knowledge, you are well-equipped to tackle your German taxes not as a daunting chore, but as an informed participant in a system you now understand.

Frequently asked questions

The income tax rate in Germany is progressive, ranging from 0% to 45%. The rates are applied to different income brackets, with higher rates applying to higher incomes.

Taxable income in Germany is calculated by subtracting various deductions and allowances from the gross income. Deductions can include social security contributions, health insurance, and other legitimate expenses.

Yes, there are various tax allowances and credits in Germany, such as the basic tax allowance, child allowance, and special expenses deduction. These allowances can reduce the taxable income and, consequently, the amount of income tax owed.

The Solidarity Surcharge (Solidaritätszuschlag) is an additional tax imposed on income tax in Germany. It was introduced to help finance the costs of German reunification. As of my last update, the surcharge was 5.5% of the income tax amount.

Income tax returns can be filed online or on paper. The process involves providing details about your income, deductions, and other relevant financial information. The deadline for filing tax returns is typically May 31 of the following year.

Yes, certain work-related expenses can be deducted from your taxable income. These might include expenses for commuting, work equipment, and professional training, among others.

Yes, income from investments, such as dividends and capital gains, is generally subject to income tax in Germany.

Here you can find our capital gains calculator for Germany.

The “Steuerklasse” system is used to determine the amount of income tax withheld from an employee’s salary. Different tax classes exist based on marital status and other factors that impact tax liability.

Yes, if you fail to file your income tax return on time, you may face penalties and interest charges. It is essential to meet the deadlines to avoid these additional costs.

Remember that tax laws and regulations may change over time, so it’s crucial to stay up-to-date with the latest information or consult a tax professional for personalized advice.